In its study « Fleet management in Europe : Growing importance in a world of changing mobility » published last july, Deloitte focuses both on the dynamism of the fleet management sector in europe but also the changes that specialized companies face today.

Today, fleet management is a market in exponential growth, worth multiple billions of dollars. More than numbers, this sector of activity acquired a real importance while mobility, both private and corporate, is evolving at a fast pace. Uses change in the work environment: service vehicles are becoming shared assets, far from the ownership norm that was predominant until now. From the technological point of view, the development of autonomous technologies and vehicles brings its share of questions concerning the fleet management of tomorrow, but also its fair share of opportunities.

Once dominated by fleet management companies, the market is nowadays invested by new players. OEMs (Original Equipment Manufacturer) are among these new entities that play a major part in the reconfiguration of the market.

In Europe, two third of new vehicles are sold to corporate channel. According to Deloitte, by 2021 63% of new vehicle registrations in Europe will be for professional fleets: the corporate fleet management market has a bright future ahead!

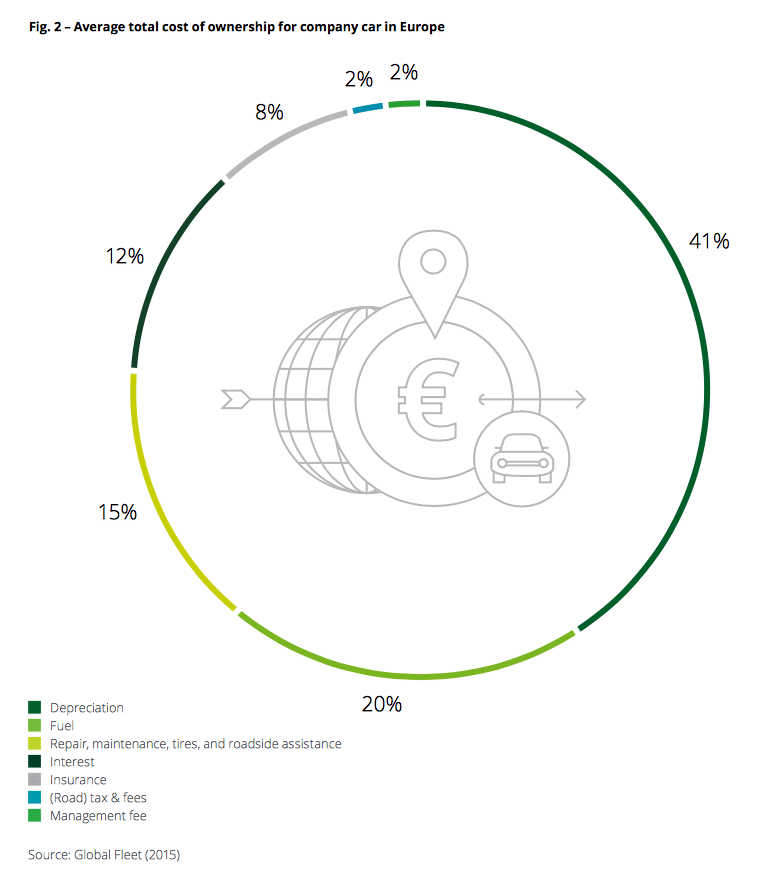

As fleets are getting bigger and bigger, companies decide to rely on external ressources to manage them. The main objectives? Optimizing the fleet’s size and reducing the overall costs associated to vehicles, the infamous TCO (Total Cost of Ownership).

Fleet management solutions are also a way to free time for the employees in charge of the vehicles, by offering services covering the entire life cycle of a corporate vehicle: the purchase itself, the additional services and the resale.

“In Great Britain, the corporate segment is expected to increase from 59% (1.3M cars) in 2012 to 63% (1.8M cars) in 2020.”

Source: Deloitte

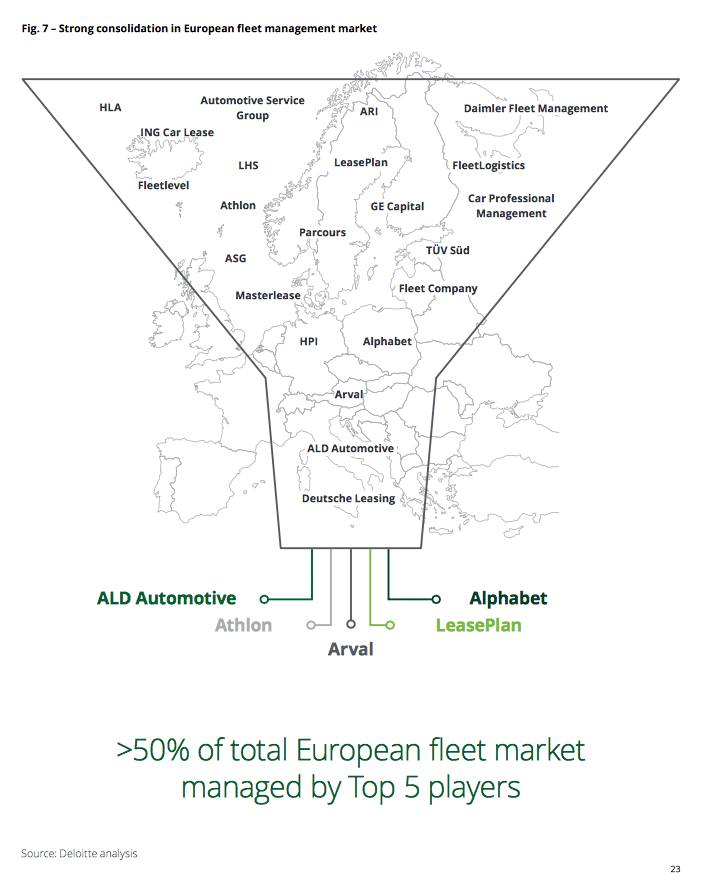

Key players in the european fleet management market

The Deloitte’s study notes three distinct types of players on the european fleet management market.

– Bank-backed fleet management companies : Arval (BNP Paribas), ALD (Société Générale) and LeasePlan (LP Group B.V)

– Companies owned by OMEs: Alphabet (BMW), Athlon (Daimler) or more recently Free2Move (PSA)

– Startups specialized in fleet management and mobility services

The top 5 players in europe (Arval, ALD, LeasePlan, Athlon et Alphabet) own more than 50% of the market. The market is consolidating more than ever. It is also very interesting to notice the numerous partnerships between these historical entities and smaller structures that can bring additional services (ride-hailing, car sharing…) on the table as well as a different vision of user experience.

From TCO to TCM: the new functions of the fleet management solutions’ provider

Today, new mobility habits slowly but surely transform the TCO (Total Cost of Ownership) into a TCM (Total Cost of Mobility).

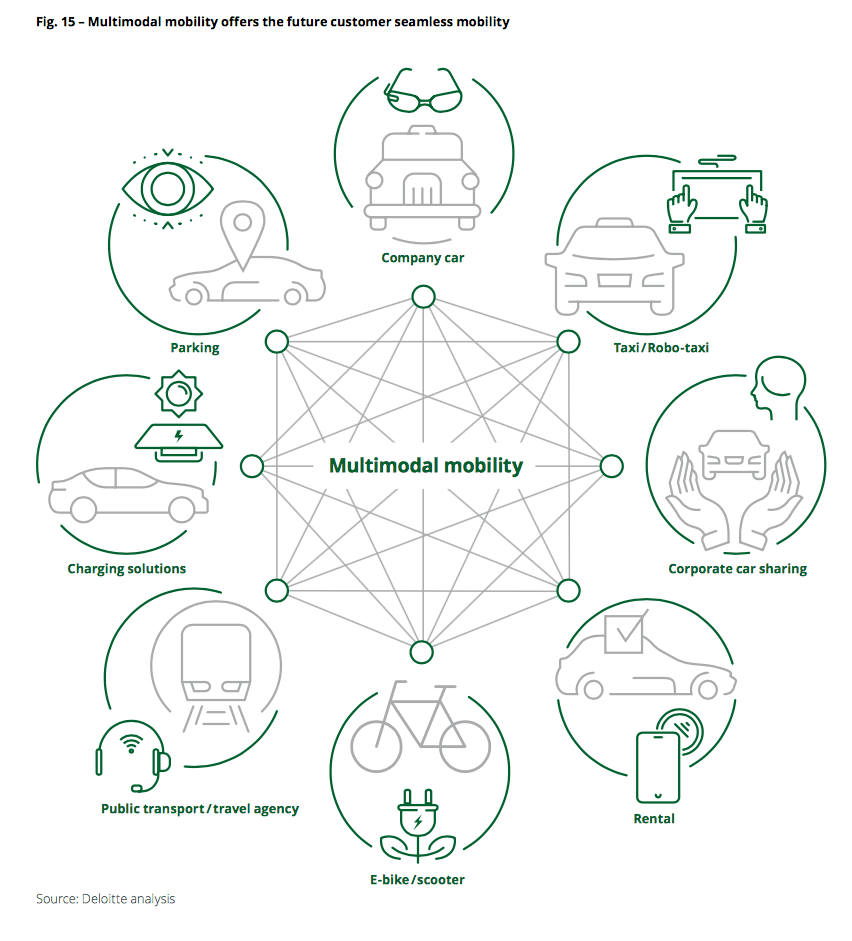

The main difference between the two? The TCM takes into account additional means of transportation, other than the individual car, such as taxi, flights or carsharing. Welcome to the multimodal mobility age!

Thus, fleet management companies go beyond their core activity, the sore vehicle’s management, to become real advisers for their customers’ global mobility.

A necessary development to adapt, other among things, to environmental regulations and generational preoccupations.

Evolution of the fleet management approach

1. Financing-related services (financing, leasing)

2. Vehicle-related services (maintenances, tires, fuel card, accident management…)

3. Driver-related services (multimodality, corporate car sharing, travel card…)

To a more sustainable corporate mobility

In addition of a required business plan evolution to meet new expectations (especially regarding digital uses) fleet management companies also have to take into account new regulations that directly impact their activities.

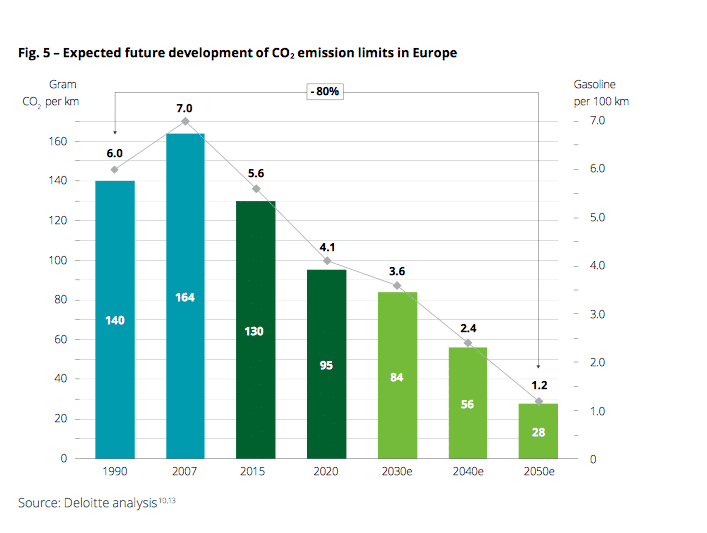

Among the most important issues raised these last few years, the reduction of greenhouse gas emissions is one of the regularly discussed about.

The european union came to an agreement to cut CO2 emissions by 80% by 2050, compared to the base year of 1990.

To reach this ambitious objective, limit values for the CO2 emissions of new cars have been established (95 grams/ CO2 per kilometer by 2020, ~84 grams by 2030 and ~56 grams by 2040.)

The consequences of these new regulations? A change of typology in corporate fleets with a growing portion of vehicles with low emission rates (hybrid, electric or using hydrogen). But also the increasing implementation of shared mobility services aiming to reduce the number of vehicles on the road.

New mobility habits: the carsharing example

Europe accounts for about 50% of the global carsharing market: the number of carsharing services’ users should grow further to almost 16m users by 2020.

And corporate carsharing progresses fastly in professional fleets. Deloitte already pointed out that fact in a previous study, The Future of Mobility.

Carsharing is presented as a logical step between the private ownership of the vehicle and the convergence between shared mobility and autonomous technologies.

New on-board technologies as well as advanced telematics give the possibility to companies to transform their corporate vehicles into a shared and innovative mobility service.

The main benefits being an optimization of the fleet’s size, a diminution of the carbon footprint as well as a consequent savings on the total cost of ownership.

Corporate carsharing: a mobility made for the Y generation

The Y generation, born between 1977 and 1994, is less interested in owning a vehicle than having the possibility to use one depending on their needs. The two keywords are connectivity and practicality.

Tomorrow, companies will be asking more and more often statistical analyses of their fleets in order to optimize them in the best way possible. These accurate and numbered observations of the fleet’s activity will also bring an increasing customer demand for multimodal mobility services, that can answer perfectly to the habits of the employees. Shared mobility services are already included in that mobility ecosystem. The fleet manager will no longer be a vehicles managers, but rather a mobility solutions provider. And fleet management companies on the market are here to help them during that transition!